To rent or to buy is almost as crucial as the age old question - ‘to be or not to be?’

There’s no single answer to the question ‘Should I rent or buy?’ You have to look at whether renting or buying an equivalent home is cheaper but a handful of shifting factors can also influence your answer, many of them are out of your control, like the direction of the housing market, interest rates and returns on investment.

When comparing the two options, renting can often come out ahead, at least compared to the early years of a home purchase. But owning a home is more ‘slow and steady’, a marathon instead of a sprint. The virtues of buying grow when you stay in a home for a while. As the years pass and your home’s equity and value have a chance to build, less of each bond payment is used to pay off interest and more goes toward your principal.

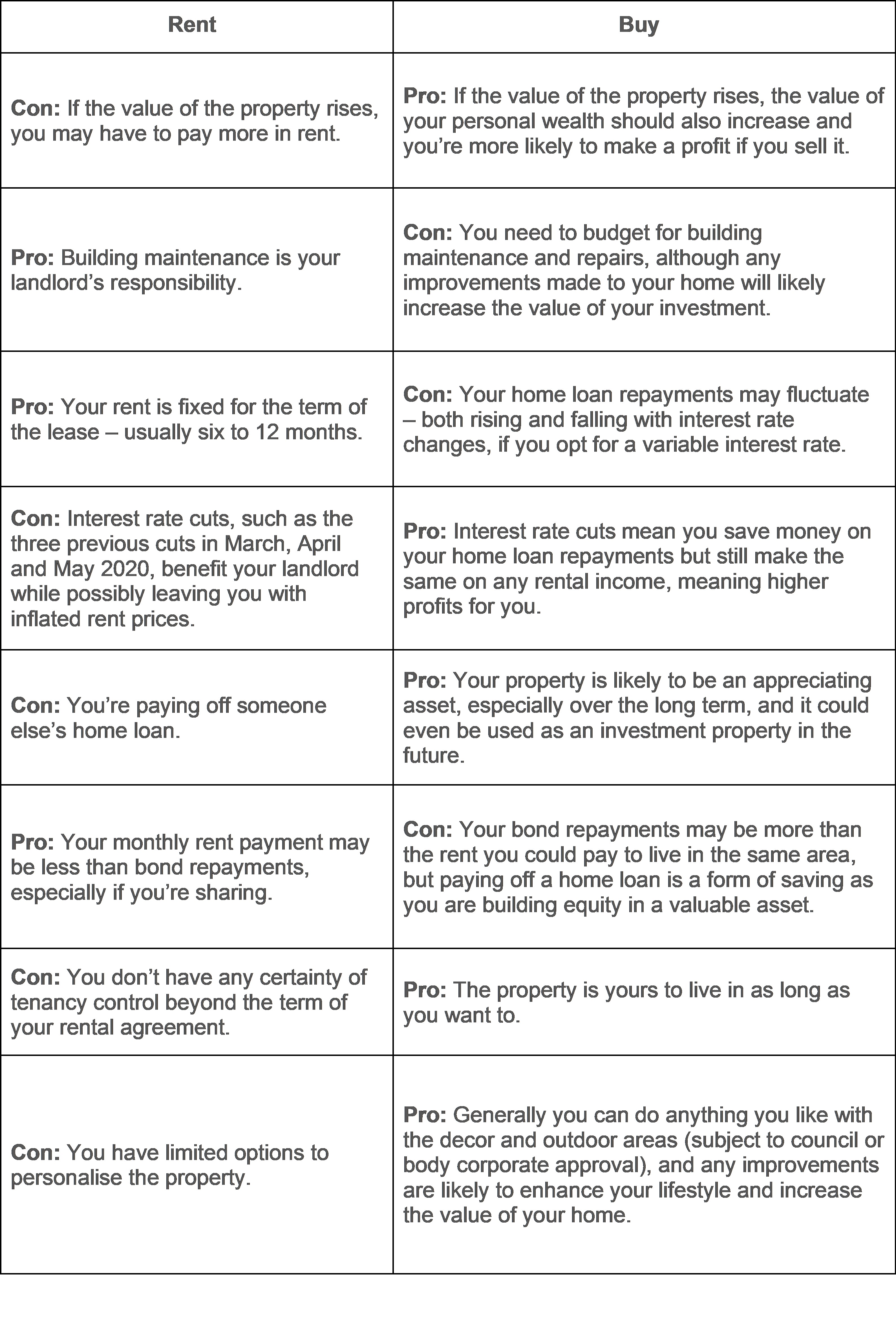

So let’s look at the pros and cons of renting and buying.

Source: Ooba ─ Renting vs buying

You may be thinking, after the year we’ve had, why would we even attempt to answer this question? Well, with the onset of the Covid-19 pandemic and the shifting market conditions, we’ve had a few interest rate cuts this year. As it stands, we’re at 7% prime lending rate, the lowest it has been in almost 50 years. So the answer to the question may very simply be buying is the better option at the moment.

If you need to move often due to the nature of your work or if sticking to one spot for at least 5 years at a time isn’t for you, renting would be a better option for you. Contracts are usually for 6 or 12 months and in some cases even month to month. If you’re not interested in maintaining or fixing up the place you’re living in, buying may be out of the question as well. Expenses for homeowners can add up quite quickly when considering initial transfer and lawyer fees, rates, levies, insurance and of course fixing up and maintaining anything that needs attention.

The long-term costs of both renting and buying need to be considered. Rental costs often accumulate and are higher than the costs involved in home loan repayments. This is because there is never an end to large monthly payments with renting, and the amount will continue to increase as time goes on. However, a home loan will eventually come to an end, which means the buyer will no longer have to make large monthly home loan payments. This is why renting is more often than not seen as a viable short-term option and buying is a long-term investment option.

When looking at the two options as a whole, the costs involved is an important aspect, but your decision will also largely rest on the security home ownership offers compared to the freedom of renting, and which of these suit your needs. With all things considered, the decision to rent or buy is also a personal one as it comes down to whether you as an individual want to commit to renting or buying a property.

Have you entered the property market? Or are you sticking to rent? Join our members group on Facebook and share your stories with us. We’d love to hear from you!

***

Please remember that it is up to each one of us to do our part and keep ourselves and loved ones safe. Visit https://sacoronavirus.co.za/ for more information about the current pandemic.

At bsmart we help our members save, and pay out cash-back bonuses every three months or annually. To learn more about bsmart contact us or click here to sign up directly through our website.